This blog post is a summary of the webinars from March 4th, 2021 and includes last valid adaptations from the European Commission from June 4th, 2021.

The Paris Climate Agreement of December 2015, is the basis for the EU taxonomy regulation which pursues three goals:

- Participating states set themselves the global goal of limiting global warming to “clearly underneath” two degrees Celsius compared to the pre-industrial era, with restrictions on a limit of 1,5 degrees Celsius.

- The ability to adapt to climate change should and will be established as a legitimate goal in addition to reducing greenhouse gas emissions.

- Furthermore, the flow of funds is to be brought in alignment with the set climate goals

What is the EU Taxonomy?

The EU Taxonomy Regulation is a classification tool that defines which economic activities are sustainable. The regulation has a direct impact on companies and investors in the areas of reporting and disclosure of financial statements in addition to environmental labels and standards (e.g. green bonds). On the one hand, the regulation intends to prevent “green washing” and on the other hand it sets out to support investors to identify “green” investments. The flow of capital will therefore be controlled accordingly. The EU taxonomy is a classification system for evaluating sustainable economic activities in all sectors including real estate. The aim is to identify and provide taxonomy-compliant activities, such as real estate investments on the market, which will also be considered “sustainable financing instruments” in the future. Ultimately, this should preserve or even increase the value of real estate. Through the definition according to the EU taxonomy it is clear which economic activities can be classified as sustainable and makes sustainability objectively measurable.

In order to obtain an alignment of taxonomy-conform assets and portfolios, undertaking an early screening of taxonomy requirements is suggested. The EU taxonomy was designed as a dynamic, i.e. evolving classification system. Due to real estate development processes spanning over multiple years, requirements for design and construction activities must be defined in the early project phases, keeping more stringent future taxonomy requirements in mind. For example, a climate risk analysis could show that increased heavy rain is to be expected at the location in the future. Hence, for unrestricted future use of the asset, the drainage system should be dimensioned in the design phase of the new construction activity in such a way that CAPEX measures can be avoided for relatively new assets. The risk of devaluation of the property in the form of a “brown discount” can then be prevented.

Effects of the EU Taxonomy

Directly affected by the regulation are financial market participants who offer financial products in the EU, including investment funds, portfolio managers as well as the area of operational pension schemes, as well as financial and non-financial companies that fall within the scope of the directive on the disclosure of non-financial information (NFRD), as well as the EU Member States and the European Union itself. These stakeholders are legally required to report on their taxonomy-aligned economic activities.

In addition, a wide range of companies, products and/or economic activities which are not legally required to report could still be indirectly affected. This is especially true for real estate developers which intend to “exit” the asset to a real estate portfolio with specific sustainability requirements (e.g. “green fund”): the investor – including her financing institution – will be interested in making a taxonomy-compliant investment, since a non-taxonomy-compliant property would reduce the degree of conformity of the overall portfolio.

Financial market participants are expected to provide initial reporting as required by the taxonomy regulation by the first quarter of 2022, reporting on the financial year of 2021.

EU taxonomy advisors & auditors

A few weeks ago, ÖGNI – the Austrian Green Building Council – was the first European Green Building Council to train professionals and credential participating individuals as so-called “EU Taxonomy Advisors approved by ÖGNI”. These professionals are trained to carry out assessments for single assets but also portfolios in accordance with the EU taxonomy regulation. An evaluated asset including results of the assessment is then subject to an independent, third-party conformity test. This is an already established process for green building certification systems e.g. with DGNB building certifications. This procedure provides quality assurance, guarantees an independent review and thus, serves as a validated evaluation of a taxonomy-aligned activity. In addition, EU taxonomy auditors are available to provide advice and support during the conformity assessment process. For this purpose, identified measures can be established. In addition, synergies with green building certifications may be pursued.

The taxonomy assessment begins in a first step with a plausibility analysis and proof of documentation of individual properties or portfolios for conformity with the EU taxonomy. The result then shows whether conformity is achieved . In the event that an asset does not achieve conformity, further measures are taken:

Step 1: Assessment of the property and gap identification to achieve requirements set forth by the taxonomy regulation

Step 2: Creation of optimization measures

Step 3: Consultation during the implementation of identified measures

Step 4: Verification and proof of documentation of individual properties or portfolios for conformity with the EU taxonomy

Step 5 (optional): Submittal for conformity check to ÖGNI or other independent institutions for third-party review to confirm conformity of the economic activity

Step 6: Reporting of taxonomy alignment

A major challenge for existing buildings is to comply with the stringent requirements and to comply with the contribution to climate change mitigation (primary energy demand as a benchmark) or climate change adaptation. If future climate scenarios as per IPCC indicates risks, measures have to be implemented to reduce such climate risks. If applicable, climate risks must be considered in CAPEX planning.

In addition, challenges exist due to non-existing or – in some cases – unrealistic and unproven benchmarks for primary energy demand. Data availability and quality can be an issue in some cases, as assessments carried out by a market analysis have shown. Find out more about the EU-Taxonomy Study here.

Generally speaking and not only applicable to existing buildings, it is necessary to comply with national NZEB standards, which in turn requires to know which different NZEB requirements exist in different EU member countries. In addition, some Eastern European countries document relatively poor primary energy factors, which means that even modern, energy-efficient buildings, which are sometimes better than the current state of the art, do not meet national NZEB requirements and can therefore not be taxonomy-compliant.

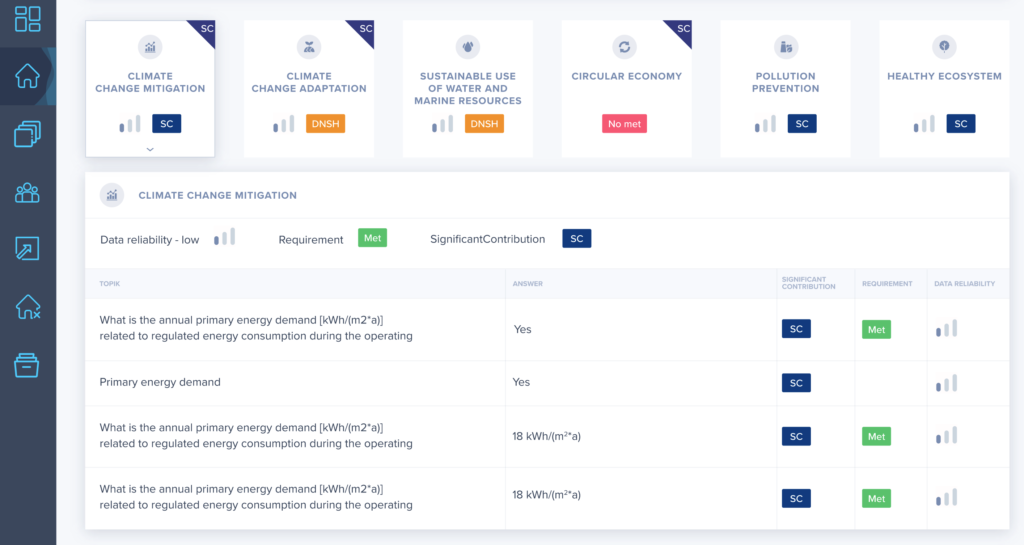

Criteria

The EU taxonomy sets out specific criteria and technical challenges. Six environmental goals and their criteria depend on the life-cycle stage of the building. This means that criteria new buildings, modernizations and existing buildings may vary across the assessments. Currently, two out of six environmental goals define what is considered to be a significant contribution (“Significant Contribution”), namely for climate change mitigation and for climate change adaptation. The definitions of the significant contribution in the other 4 environmental goals – protection of water and marine resources, the transition to a circular economy, prevention and reduction of environmental pollution and protection and restoration of biodiversity and ecosystems – will follow.

Material testing in regards to SVHCs (substances of very high concern) has proven to be a technical and practical challenge. The matter is complex because the regulation refers to different EU directives and various market participants are currently verifying to what extent this requirement is realistic and feasible in practice. In addition, for some requirements there will have to be close coordination between tenants and real estate developers as certain decisions can fall in the scope of both. This suggests that green lease agreements will become a more important tool in the years to come.

For example, hotel operators may have their own specifications for water fixtures. According to the legal act, a maximum water flow of only eight liters per minute applies to showers. (Note: Residential buildings have been exempted from water flow restrictions in the current act).

EU Taxonomy Requirements

According to the delegated act, an economic activity is considered to be taxonomically compliant if a significant contribution is made in at least one of the six climate goals and, in addition, no significant harm is caused in any of the other five defined climate goals, and any minimum requirements relating to human rights, labor standards as well as technical evaluation criteria have been met and implemented.

Assets in planning and under construction

For the properties in planning, a future-oriented implementation of measures to achieve taxonomy conformity is necessary with immediate effect, in order to ensure an alignment when the real estate project is completed and handed over. It is recommended to check the properties currently during the design and construction process for conformity as soon as possible and, if necessary, initiate processes for optimization. Complete compliance with the taxonomy without specifying requirements at this stage is considered unlikely.

DGNB certification and EU taxonomy

Many of the DGNB certification criteria already correspond to the criteria of the EU taxonomy. DGNB is currently working on a system update so that the EU taxonomy can be fully implemented in the green building rating system in the future.

Assessment Fees

Generally speaking, the EU Taxonomy regulation does not require an independent consultant to perform the analysis. However, many organizations required to report on taxonomy alignment do currently not have the internal resources to rate their economic activities for compliance.

Fees for the assessment by a consultant depend on the scope of the assessment and are calculated individually. A large number of factors can influence the costs of the assessment, e.g. is it a pure plausibility check or an on-going consulting of a project spanning over multiple years, or are additional services in the form of evidence to be provided. The Austrian Green Building Council ÖGNI has established a fee schedule similar to a green building certification fee..

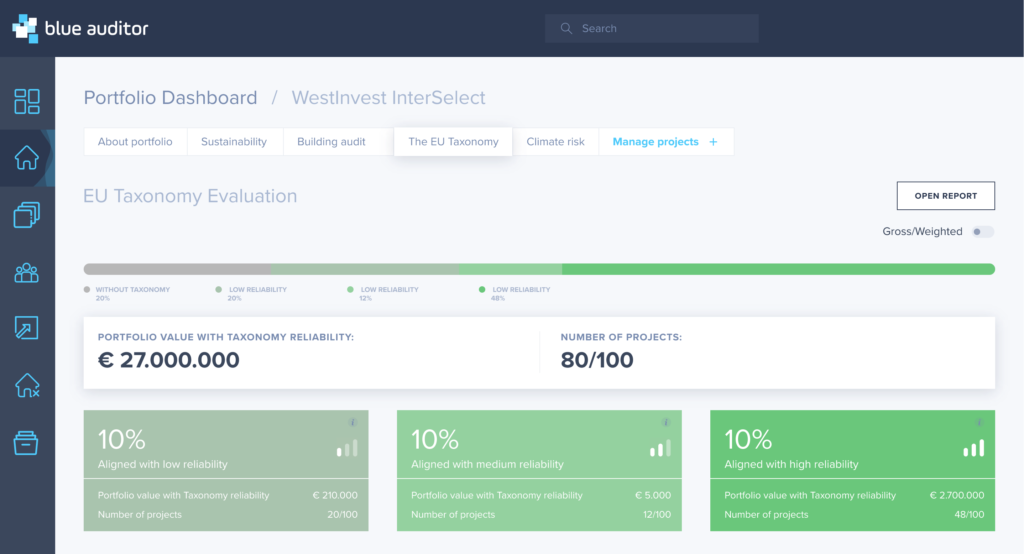

For taxonomy compliant reporting, blue auditor has fully implemented EU taxonomy assessments for individual real estate assets as well as portfolios allowing developers, consultants and asset managers to rate their economic activities according to the delegated act.